Sales & Marketing Report 2017: The Evolving Role of TPM

We’ve been discussing trade promotion management in the pages of this report for almost a decade — can there really be anything new to discuss? It’s an established space, certainly, with a number of competent vendor tools available to consumer goods companies.

Yet it seems increasingly clear that successful consumer goods businesses must adopt and adapt capabilities to capitalize on the growing “front edge” of the consumer products industry while ensuring that the traditional base business is properly supported. The challenge for the large, traditional players is to balance protecting their base business with finding ways to capture their fair share of new growth.

While most of the air is consumed with talk of digital transformation or disruption, most current business is still conducted via conventional products through traditional retail and supported through conventional trade promotion funding. Finding ways to appeal to younger consumers through new and novel ways is important, but so is making sure that the existing business is properly served (even as it shrinks). The companies able to do this well will be the ones that thrive.

With regard to trade promotion, it still strikes me as curious how many companies don’t have a purpose-built tool or are still limping along with a homegrown, often spreadsheet-based application. We certainly see improvements based on better data and information, along with more insightful and faster analytics.

TPM remains among the more frequent inquiry topics by consumer goods companies to IDC — although over the last year or so we’ve seen an interesting shift in what they’re inquiring about. Companies that ask us about TPM are increasingly looking for effectiveness and optimization tools.

Some years ago, we were often asked whether you needed TPM before embarking on optimization. At the time, my answer was “Yes,” and that seems borne out in practice. The vast majority of consumer goods companies have trade promotion management capabilities, but they often don’t have the more advanced effectiveness of optimization tools.

Before going any further, let’s define the terms broadly:

- Trade promotion management is the basic “infrastructure,” the ability to track promotions (both completed and planned) against the available promotional budget and ensure compliance.

- Trade promotion effectiveness is the backward-looking capability to evaluate promotions and promotional vehicles for efficiency, effectiveness and performance. It’s the ability to do “post-audits,” if you will.

- Trade promotion optimization is the forward-looking capability to design and implement the best possible promotions to drive business outcomes for both the consumer goods manufacturer and the retailer.

This may seem intuitively obvious, but only a few best-in-class companies actually do all three. It’s also important to note that some vendor tools do all three, or some subset of the three.

Companies increasingly are unwilling to rip out existing IT tools, and TPM seems poised to join that trend. One manufacturer we spoke with earlier this year was quite happy with its foundational TPM tools but wanted to find optimization capabilities it could put on top of what it already had.

That relates back to another prediction we made for the industry, that within five years the majority of large consumer goods companies will have reached the point of trade promotion maturity and will be able to leverage sophisticated optimization tools. The notion of trade promotion is going to change in the coming years as direct-to-consumer and private brand growth inevitably happens. But as we noted earlier, traditional trade will persist for many years.

Trade promotion has been problematic for many companies that have less than full visibility into performance and lift, but this is changing — and has to change. The tools are available, the data is available, and within a few years we expect true optimization to be a reality (for promotion planning, execution and analytics) for all large players, as well as for many small and medium-sized ones.

As we noted last year, most consumer goods companies are now largely focused on driving promotion efficiency rather than simple cost savings (though they are quite happy if there are savings), and they’re increasingly using technology to facilitate promotion analysis and performance.

One thing that is new (or new-ish) that we increasingly hear about is the issue of analytics capabilities. While consumer goods companies don’t have 100% of the data they need for comprehensive analysis, the amounts and quality of what they do get are much better and the analytics, therefore, play a larger role.

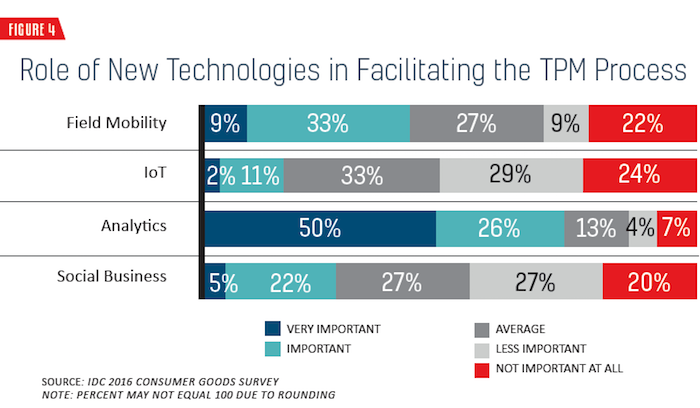

Given this concern about data and analytics, we specifically asked a question last year about the role that a few “new” technologies might play in driving better promotional performance and, perhaps, as harbingers of things to come. The results of that question are presented in Figure 4.

In conversations we’ve had this year, analytics remains the clear leader in terms of impact on the trade promotion process. Field mobility is critical for retail merchandising and promotional sets, and we’re seeing it become even more important for the actual trade promotion process. As we move forward toward a greater role for consumer interactions, this may change. But, for now, it’s still early days.

We are fielding many more questions this year about the role for the internet of things, or sensors primarily, and its potential impact on the trade promotion process. While that impact is clearly more on the physical execution of promotions rather than the planning or financial aspects, the reality is that it ultimately becomes just another source of data available to the analytics engine — thus, emphasizing the importance of those analytics.

Turning to the future, we reiterate a question from last year: If we are on the verge of a completely new model of consumer engagement, what does that mean for trade promotion? It’s important to “ground” this comment at the outset. While growth may be through omnichannel, direct-to-consumer and highly personalized interactions, the majority of the purchase base still happens through traditional retail and will for some time. But the writing is on the wall, particularly as younger generations of consumers come into the marketplace; they’ll have no patience for “old-fashioned” forms of commerce.

In the near term, we’re going to see new technologies increasingly applied to existing TPM process competency, giving way in the longer term to effectiveness and optimization. Figure 5 is an illustration of what this might look like.

But the more interesting discussion is about what the longer term looks like, where new technologies and consumer behaviors will dramatically affect the way that consumer goods companies manage and offer trade promotions. What happens to funding in an omnichannel world? As we said in the introduction, it’s not a big deal when direct-to-consumer sales are in small single digits, but what happens when they become a significant percentage of total sales and a significant portion of the annual trade promotion budget no longer supports traditional retail sales?

Here’s one possibility: As products and the shopping experience become more personalized for specific consumers, the promotional process also becomes more personalized. The notion of a hyper-refined promotion — while not possible today — may become the way in which companies engage with consumers — at least in part.

Another implication for TPM/TPO is the reality of “always on.” The ubiquity of smart devices and digitally enabled consumers means that commerce is 24/365. The promotional process will have to adapt, either in terms of how offers are presented, or in how demand fluctuations drive hyper-refined promotions.

_____________________________________________

To read the rest of the report, click on the links below:

- Sales & Marketing Report 2017: Editor's Note

- The Progress Report

- The Evolving Role of TPM

- What to Do with Data

- Is DTC the Future — or the Present?

- Taking the Risk Out of Digitization

- Building a Smart Digital Enterprise

To download the full report, click here.