Analytics Study 2017: Retail

Analytics Transformation Mid-Stream

The retail industry is in an analytics arms race. May the best insights win

Customer-centricity and the rise of digital commerce, led by Amazon, has pushed retailers to collect and measure more data than ever before. Many are in the midst of a cultural and technical transformation, shifting toward a more analytics-driven approach to how they manage their businesses. Along with such a dramatic change are inevitable delays and hurdles, with the ability to attract the right analytics talent leading the list.

The good news is that retailers are making real progress and gaining ground on the competition.

Progress on All Fronts

Companies investing in analytics for the long haul know it all starts with a solid foundation: clean data, robust tools and good governance. It’s not sexy, but it’s essential to support analytics applications that will deliver accurate, meaningful insights and true ROI.

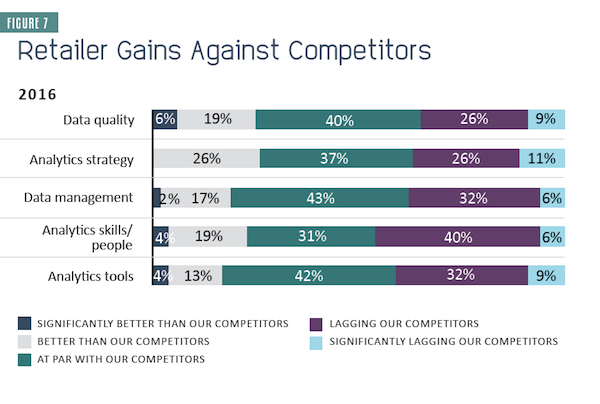

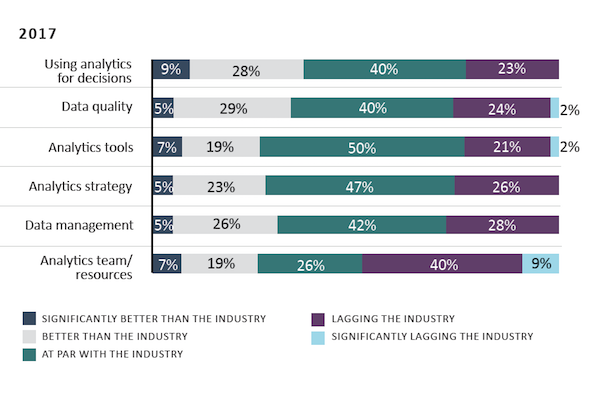

Retailers have spent the last year making those needed investments (Figure 7). They’ve made progress across the board, with the biggest gains ― the number of retailers saying they are now better or significantly better than the industry ― coming in data management, data quality and analytics tools. This year’s survey also asked about retailers’ ability to use data to make decisions, and found a healthy 37% besting the competition. At the other end of the spectrum, most respondents have pulled themselves out of the “significantly lagging” category across capabilities.

But progress against Amazon is little changed over the past year ― except for a small group who now call their analytic capabilities significantly better than Amazon’s. Amazon continues to push the bar aggressively forward, making even achieving par a significant accomplishment. While some retailers collect detailed data as part of the sales process, such as furniture dealers, “It is possible that this represents retailers across a wide variety of business models,” says Ken Morris, principal, Boston Retail Partners. “Innovative or digitally native companies (e.g., Zappos, Bonobos) are more likely than established brick-and-mortar retailers to have effective analytics capabilities.”

Like retailers, Jeff Roster, VP of retail strategy for IHL Group, considers Amazon the gold standard for analytics skill. “Until retailers can offer their customers perfect inventory visibility, tracking of all orders and a seamless customer experience in-store, they will be behind. That is where the focus will be for the next three years.”

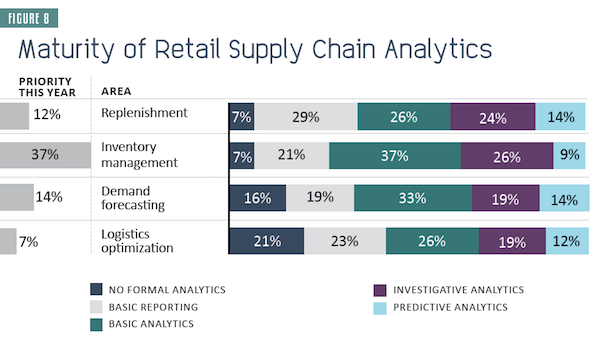

Advanced Supply Chain

Retailers’ supply chain analytics capabilities are the most mature (Figure 8) and retailers are most likely to be using investigative or predictive analytics in this area. This includes demand forecasting, a merchandising discipline used to direct supply chain management and execution, as well as replenishment, an area which has seen heavy retailer investment over recent years. In addition, inventory management continues to be a high priority.

“Our research shows a majority of retailers are in the diagnostic phase of advanced analytics maturity,” says Robert Hetu, research director, Gartner Retail Industry Services. “This is the second of the four-stage maturity: descriptive, diagnostic, predictive and prescriptive.”

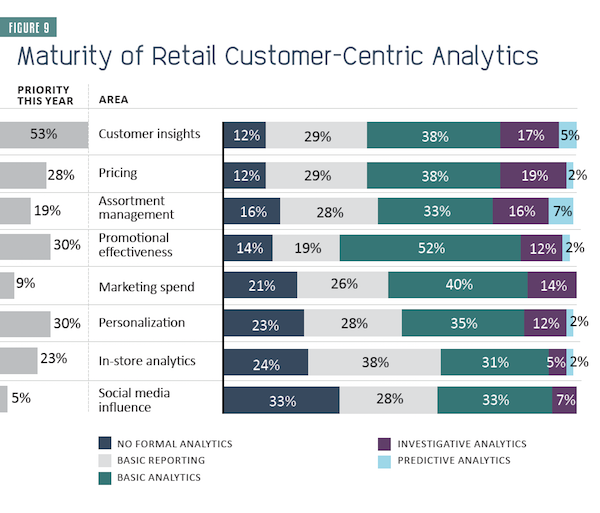

Marketing and merchandising analytics capabilities lag those of supply chain, with the move toward more advanced capabilities very much a work in progress (Figure 9). As retailers’ focus shifts more sharply to being customer-centric, they are seeking similar levels of investigative and predictive analytics capabilities for these functions. Customer insights tops retailers’ analytics priorities this year (53%), followed by personalization and promotion effectiveness (30% each).

One reason for supply chain’s relative maturity is the availability of solutions in those areas. Major vendors started in financials and supply chain ― and benefited from the horizontal nature of those solutions. As solution providers build out merchandising, marketing and other customer-centric analytics tools, retailers will more easily adopt those capabilities.

Top Challenges

As Figure 7 illustrates, retailers have made progress in the maturity of their analytics team/resources; 19% say they are better than the industry, and 7% rate themselves significantly better. But they still call inadequate talent or dedicated staff their biggest analytics challenge (56%, in Figure 2 of overview section).

This suggests that while progress has been made, as retailers have pursued analytics talent they have also seen how difficult it can be to assemble the ideal complement of skills, tools and data governance. However, as seen in Figure 3 in the overview section, retailers’ plans to fill specific analytics positions are anemic at best, suggesting they are still not confident on how to organize and properly staff this key function.

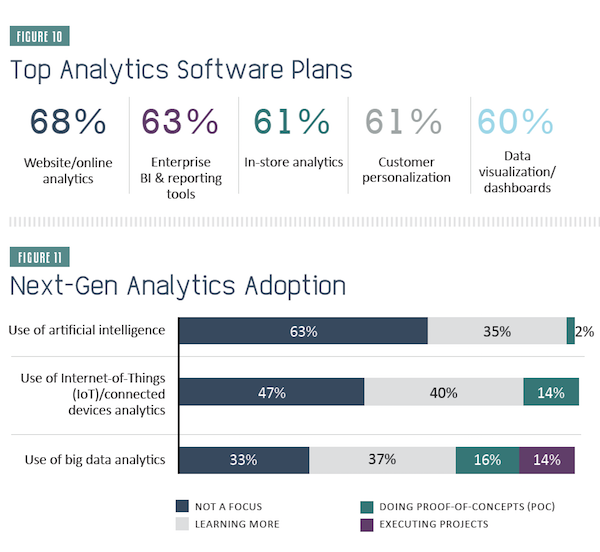

Limited software toolsets and the inability to integrate data from multiple sources are the next biggest analytics challenges for retailers (47% each, in Figure 2). But the indicators are much stronger here for intent to solve these issues than for filling the talent gap. More than half of retailers intend to add for the first time, upgrade or change suppliers for a long list of analytics application areas (Figure 10). And lack of intent to make changes may just mean they have already checked those boxes. Investment plans appear quite healthy, with retailers prioritizing web/online analytics, enterprise BI & reporting tools and in-store analytics for their spending this year.

Budgets and Vendors

Budgets also reflect retailers’ focus on continuing to strengthen their analytics chops; while they devoted an average 10.5% of IT budgets to analytics in 2016, they project that climbing to 16.6% by 2021, a CAGR of 12.1%.

Retailers are split nearly 50/50 on whether they currently, or plan to, turn to outsourced resources to conduct data analytics vs. building out this capability completely in-house.

IHL Group’s Roster sees outsourcing as a key strategy to help retailers overcome their staffing issues. “I don’t believe it’s a requirement for many retailers to have data scientists on their teams,” he says. “I do think it’s mission critical though to have access to that expertise. We’re seeing a rapid scale up of service providers offering this capability.”

A portion of retailers’ IT budgets must be carved out for forward-looking applications of analytics (Figure 11). Big data has seen the most progress so far: 14% are already executing projects and 16% are in the proof-of-concept phase. Applying analytics to data from the Internet of Things, connected devices and artificial intelligence are at earlier phases of education and adoption.

IoT will dramatically increase the data available for customer insights. “With this explosion of data, it is even more critical to understand decision modeling — identifying what data actually drives key decisions and what data is merely excess noise,” says Morris. Other analytics trends to watch include graph databases, cognitive capabilities, open source analytics platforms and the impact of cloud-based POS to enable real-time analytics.

It’s difficult to underestimate the importance of robust data management and a strong analytics focus to the future of retail. Omnichannel and brick-and-mortar retailers are being challenged by pure-play retailers built from the ground up based on these competencies, as well as consumer goods companies with a longer track record in analytics pushing for direct and sometimes transactional relationships with consumers. All are continuing to work at establishing and maintaining the analytics talent, tools, structure and culture that will allow them to remain competitive in the new, insights-based, customer-centric retail marketplace.

________________________________________________________________________

TABLE OF CONTENTS

- Analyst's Note: The Great Analytics Divide

By: Gaurav Pant, Chief Insights Officer, Incisiv

- Overview: Analytic Growing Pains

Retail and CG companies struggle to get the right people, governance and technology.

- Retail Section: Analytics Transformation Mid-Stream

The retail industry is in an analytics arms race. May the best insights win.

- Supplier Section: The Bar Keeps Getting Raised

CG companies are struggling to keep up with the data-driven market leaders.

- Click here to Download a PDF of the FULL STUDY